AMERICAN TAX PLAN REFORM

“It is a great paradox that today taxes are too high and state income is too low , and the most efficient way to increase the state income, in the long term , is to cut taxes as soon as possible.”

These are John Fitzgerald Kennedy words during his speech in Wall Street on 1962.

The same theory had been stated by John Maynard Keynes in 1933.

President Trump signed the “Tax Cuts and Jobs Act” into law on Dec. 22, 2017.

The law will lower business and individual tax rates, modernize US international tax rules, and provide the most significant overhaul of the US tax code in more than 30 years.

Corporate Tax Rate

The law creates a single corporate tax rate of 21%, starting in 2018, and repeals the corporate alternative minimum tax. Unlike tax breaks for individuals, these provisions do not expire. The top corporate tax rate is currently 35%, the highest rate of any large, developed country. Combined with state and local taxes, the statutory rate under the new law will be 26.5%, according to the Tax Foundation.

Immediate Expensing

The law allows full expensing of short-lived capital investments — rather than requiring them to be depreciated over time – for five years, but phase the change out by 20 percentage points per year thereafter.

Pass-through Income

Owners of pass-through businesses – which include sole proprietorships, partnerships and S-corporations – currently pay taxes on their firms’ earnings through the personal tax code, meaning the top rate is 39.6%.

The law creates a 20% deduction for pass-through income. Certain industries, including health, law and financial services, are excluded from the preferential rate, unless taxable income is below $157,500. The deduction is capped at 50% of wage income or 25% of wage income plus 2.5% of the cost of qualifying property.

Interest

The net interest deduction, which currently has no cap, will initially be limited to 30% of earnings before interest, taxes, depreciation and amortization (Ebitda). After four years, it will be capped at 30% of earnings before interest and taxes (Ebit).

Cash Accounting

Businesses with up to $25 million in average annual gross receipts over the preceding three years will be eligible to use cash accounting, up from $5 million under current law.

Net Operating Losses

The law scraps net operating loss carrybacks and caps carryforwards at 90% of taxable income, falling to 80% after 2022.

Foreign Earnings

The law enacts a deemed repatriation of overseas profits at a rate of 15.5% for cash and equivalents and 8% for reinvested earnings.

Companies with over $500 million in annual turnover are subject to the base erosion anti-abuse tax (BEAT), which is designed to counteract base erosion and profit shifting, a tax-planning strategy that involves moving taxable profits made in one country to another with low or no taxes. BEAT is calculated by subtracting a company’s regular corporate tax liability from 10% of its taxable income, ignoring base-eroding payments. Tax credits can offset up to 80% of BEAT liabilities.

Foreign-derived intangible income (FDII) refers to income from the export of intangibles held domestically, which will be taxed at a 13.125% effective rate, rising to 16.406% after 2025.

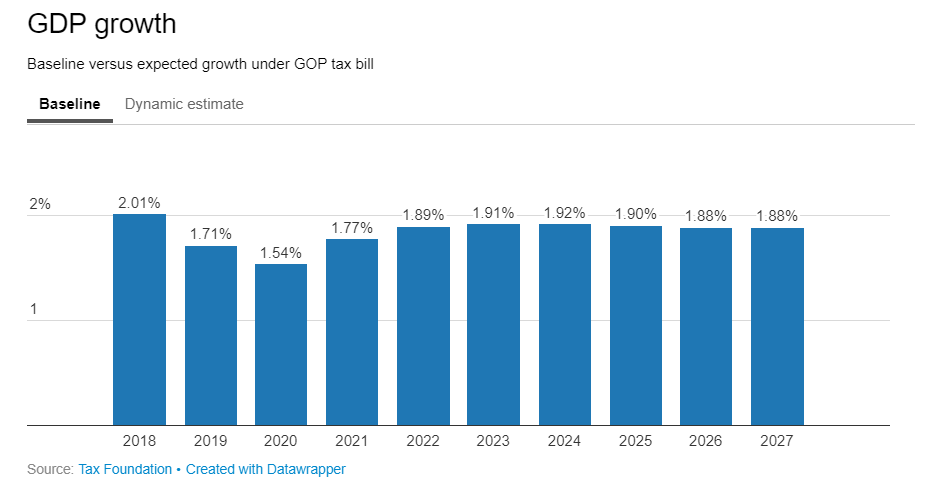

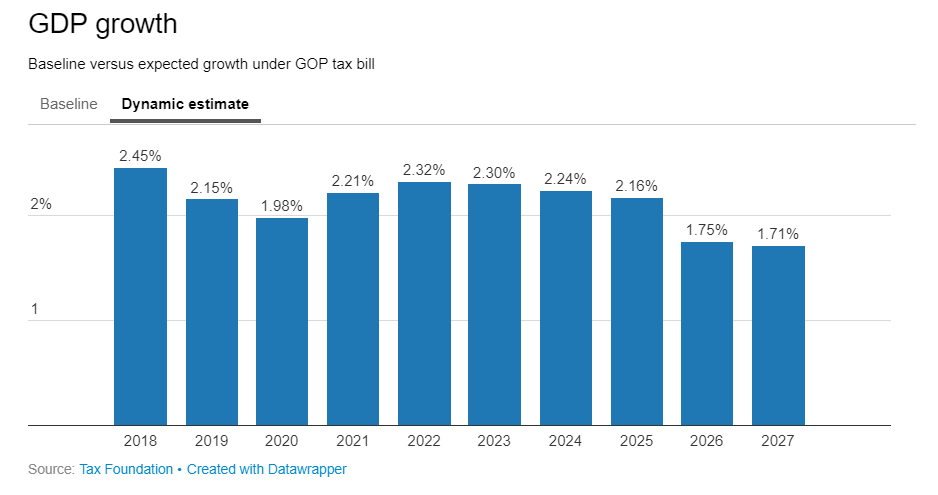

The Tax Foundation forecasts a 1.7% increase in long-run GDP, clarifying that most of this extra growth is likely to be front-loaded: “Economic growth is borrowed from the future, but the plan, in aggregate, still increases economic growth over the long run.”

Sources : pwc.com – investopedia.com – kpmg.com – taxfoundation.org

DISCLAIMER

This publication must not be regarded as offering a complete explanation of the investment matters that are contained within this publication.

Authors are not responsible for the results of any actions which are undertaken on the basis of the information which are contained within this publication, not for any error in, or omission from, this publication.

The authors expressly disclaim all and any liability and responsability to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.