MADEIRA, FREE TRADE ZONE

The Portuguese gorvernment has created two (non-offshore) free trade zone : the Madeira International Business Center and the Santa Maria Island Free Trade Zone.

The FTZs offer advantages including corporate tax rate of 5% for profits realized with entities not Portugal-based no property transfer tax, no tax on capital gains dividends remitted to a company based in EU/EEA or a country with a DTA treaty with Portugal and 50% reduction of taxable income for qualifying companies.

To qualify for these tax deductions, companies must obtain a license by either investing in Madeira at least Euro 75,000 on a two years period resulting in one job created or creating at least six jobs in Madeira ; the corporation licensed before December the 31st 2014 are guaranteed the listed fiscal advantages until 2020.

The new regime applies until 31 December 2027 for entities licensed to operate in the MFTZ from 1 January 2015 through 31 December 2020. Entities licensed to operate in the MFTZ under the previous regime also may apply for the new regime, provided the relevant requirements are met. An application for a license must be submitted (in Portuguese) to the Madeira Development Company to operate in the MFTZ and qualify for the benefits discussed below.

Reduced corporate tax rate

As under the previous regime, entities licensed to operate in the MFTZ are subject to Portuguese corporate tax at a rate of 5% (one of the lowest rates in the EU) on eligible taxable income and gains. The new regime sets limits on the benefits to be granted by imposing “ceilings” of taxable income on which the 5% rate is applied.

The ceilings are based on the number of jobs created (the number of jobs required to be created remains unchanged). A (new) cap also is set on the tax benefits, at one of the following amounts: • 20.1% of annual gross value added; • 30.1% of annual personnel costs; or • 15.1% of annual turnover.

Withholding tax exemption

The regime provides for a personal income tax or corporate tax exemption for nonresident recipients of dividends/profits and interest (or other forms of remuneration) on shareholder loans (as well as allowances or capital advances) paid to shareholders of MFTZ entities, provided the shareholders are not resident in listed tax haven jurisdictions. These exemptions do not apply to Portuguese resident shareholders, except for entities licensed to operate in the Industrial Free Zone of Madeira or entities carrying out air or sea transport activities.

Capital gains tax exemption

The general Portuguese corporate tax treatment of gains on the sale of shares also applies to the disposal of holdings in companies in the MFTZ and to the disposal of shareholdings held by such companies. The exemption is not available if the shareholders are resident in a tax haven jurisdiction or in certain other cases.

Tax credit

Entities licensed to operate in the Industrial Free Zone of Madeira may benefit from a 50% reduction in the amount of tax due (in addition to the 5% corporate tax rate), provided certain conditions are fulfilled, under the same terms as under the previous MFTZ regime until the end of 2020.

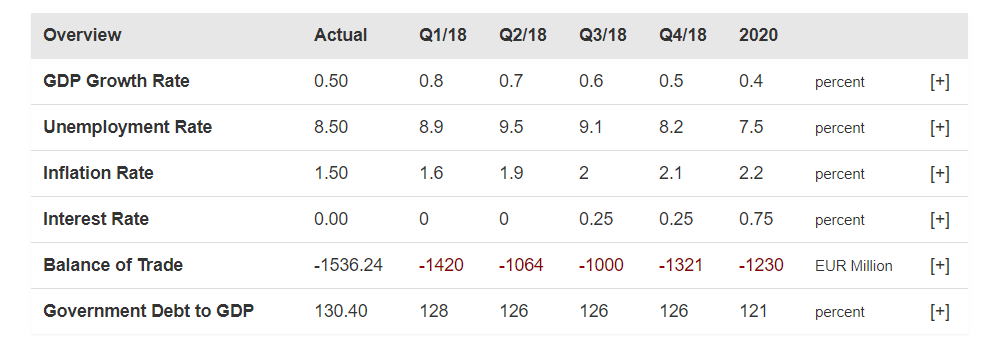

This chart has economic forecasts for Portugal including a long-term outlook for the next decades, plus medium-term expectations for the next four quarters and short-term market predictions for the next release affecting the Portugal economy.

Sources : lowtax.net – deloitte.com – healyconsultants.com – EY.com – tradingeconomics.com

DISCLAIMER

This publication must not be regarded as offering a complete explanation of the investment matters that are contained within this publication.

Authors are not responsible for the results of any actions which are undertaken on the basis of the information which are contained within this publication, not for any error in, or omission from, this publication.

The authors expressly disclaim all and any liability and responsability to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.